Health Care Reform or Massive Power Grab?

30/11/15 22:28

Originally published on August 1, 2009, this post refers to the “first look” that the public got at the health care proposal. It was only a little more than 1,000 pages and notoriously grew to more than 3,000 as it worked its way through Congress, which told us, via Speaker Nancy Polosi, that they (the Congress) “would have to pass it to find out what was in it.” Read it for yourself, as the link I included is still live.

I should start by admitting I have a bias against BIG: I don’t much care for big cities, big schools, big bureaucratic corporations, big hospitals, and — most of all — big government. My life experience has taught me that big entities beget big problems, and the bigger the problems, the more resistant they are to solutions — especially common-sense solutions.

I like small towns because problems are easier to define, and common-sense solutions seem to be easier to come by because you know whom to call, and volunteers are easier to motivate.

As an Army brat, I attended 12 schools, including 4 high schools — one big one and three small ones. As both a student then and later as a teacher, I concluded that small schools are likely to serve students and parents better than their large, bureaucratic counterparts.

Large corporations become bureaucratic, almost by definition; and bureaucracy helps to obscure bad business practices. Just look at the recent history of financial institutions that did catastrophic damage, then were deemed by government as “too big to fail,” thus necessitating taxpayer bailouts and government takeovers.

When it comes to health care, I prefer to deal with routine issues at a small private practice in the tiny Maryland community where we have a lake house: The doc listens to you and the problem gets resolved. I even made the three-and-a-half-hour trip to that community to have an angry gall bladder removed because they could take me right away, rather than wait for at least two weeks to schedule the surgery at the huge Hershey Medical Center, which is only 7 miles from my Pennsylvania home. I’m glad the med center is there when big medical guns are needed; but it takes way too much energy to get a hangnail diagnosed there.

The remedy or the disease?

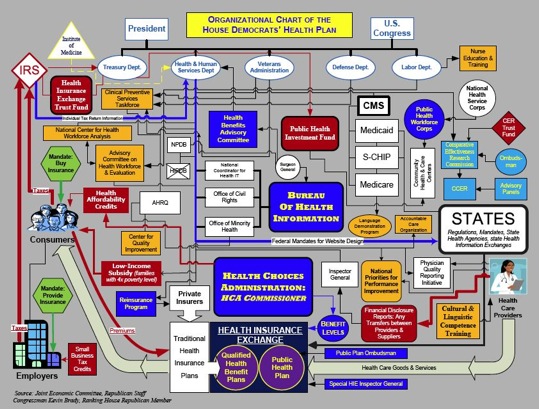

And now the Federal government, which has grown at a breathtaking pace since last fall, is poised to nationalize our health care system, according to a plan that, in effect, points to a leak in the national faucet and proposes to fix it by tearing up the entire American plumbing system. And just wait until you see the proposed bureaucratic solution. I’m certain that most Americans want health care reform that would address cost escalation, insurance for pre-existing conditions, portability, and catastrophic care. But this proposal redefines Byzantine complexity. The idea that healthcare, would become less complicated and more affordable by saddling it up this mind-numbing bureaucracy beggars belief. Take a look at how it is organized:

This diagram was created by Rep. Kevin Brady (R-Texas) and Republican staff of the Joint Economic Committee to illustrate the organization of the Democratic health care plan. It interested me because Republicans are being vilified for opposing the bill. I’m a registered Independent because neither party represents enough of my core views to strongly identify with, but on this one, I’m grateful to the Republicans for standing firm and to the Blue Dog Dems who are risking the ire of the White House in repudiating this nightmare.

Democrats have prevented Republican House Members from sending their constituents a mailing that includes this organization chart under House franking privileges, claiming that it is inaccurate. Well, I don’t think so because I’ve read the bill. In fact, I’m not sure it fully includes all of the plan’s complexity. Don’t take my word for it . . . you can read the thing yourself by clicking here.

Read the Bill!

Start by reading the Table of Contents; it is scary unto itself. Next: read pages 22-28, just to get a feel for the kinds of rules and regulations this monstrosity proposes. Lawyers will love it. Here are just a few page-by-page highlights to whet your appetite:

Page 27 covers “Health Insurance Exchanges,” which effectively brings private heath care under government control. See page 84, line 4 to see how sweeping this governmental mandate is and the potential it holds for rationing care.

Page 29, lines 4-16 establishes a cost-for-benefits ceiling (annual limitation) on “essential benefits” for what the government deems to be an acceptable plan.

Page 30, Section 123, line 11 mandates a private/public Health Benefits Advisory Committee government committee that decides what determines eligible treatments/benefits are provided by an acceptable plan.

Page 42 lays out the duties of the Health Choices Commissioner. He gets to choose your benefits, not you.

Page 50, Section 152: I’m pretty sure that the language of this section provides health care to non-US citizens, illegal or otherwise, even though another section of the bill says that it (not the section on page 50) doesn’t provide care to illegals. Consult your legal staff to find out for sure.

Page 65, Section 164 greatly expands subsidized care to retirees (55 years or older) and family members, even if they already have health plans. And wait until you read the red tape required to collect!

Page 143: Read Subtitle B of this section carefully, as it relates to “Employer Responsibility.” In it you will find that in order to “comply” employers must:

Page 57, Section 163 deals with Standardizing Electronic Administration Transactions. This looks scary to me because page 28, line 5 allows “real time determination of an individual’s financial responsibility at the point of service.” Sounds like governmentspeak for “we can get a look at your bank account.” I could be wrong. Hope so, especially since the it also enables electronic fund transfers to allow “automatic reconciliation,” which means the government now has direct access to your bank account. Imagine the outcry if George W. Bush had a bill on the Hill that would allow this level of government intrusion.

What about YOUR doctor?

Are you wondering how your doctor would be affected? Start on page 238, and I dare you to read through page 255. If you do, you’ll wonder why ANYONE would want to become a doctor (especially since the government decides on his or her level of reimbursement on page 127). My personal favorite of all the dictates is on page 253, line 10, under “Validating Relative Value Units” for doctors’ fee schedules: “Work elements to be validated include: time, mental effort and professional judgement, technical skill and physical effort, and stress due to risk.” OMG.

Page 265 covers government mandates on productivity for private health care; Page 489, Section 1308 allows the government to include Marriage and Family Therapy as a health care element; and on and on it goes. Believe me there are HUNDREDS of radical bureaucratic proposals in this bill, but I don’t have enough time to list all the catastrophes. Don’t take my word for it: Read it yourself, or to make it easier, divide it up among your friends and let them take notes, then exchange information.

Over recent months, I’ve watched as Congress and the Administration have severely limit the economic freedom of Americans by quadrupling the deficit, printing money to purchase our own debt, and delivering a pork-laden, non-stimulative “stimulus” bill, all of which are likely to prolong the recession. But in spite of this and a now-stalled cap-and-trade bill that is enough to scare the pajamas off of manufacturers from bread bakers to bomb makers, in the back of my mind I’ve believed there was still room for the private sector to restart the country’s economic engines, something that government cannot do.

An affordable bill? Not so much.

But this so-called health care “affordability” act, which will fundamentally alter one-sixth of our economy, could literally sink the ship of state. The administration says it will be revenue neutral; the Congressional Budget Office (which effectively works for the Democrats), says it will cost $1 trillion or more (think MORE) over 10 years. A growing number of Americans are seeing it for what it is: a naked government power grab based on the assumption that somehow government can do better in “caring for” people than they can do for themselves and through the private sector. This issue is far too serious to stay on the sidelines, so here are some things you can do to stop this national catastrophe:

Common-sense reform

Yes, health care needs reform badly, but let’s start with a common-sense approach that tackles the issues that drive up costs:

Get these initiatives moving, then see what a government program for uninsured Americans would look like.

Please understand that I wouldn’t have taken the time to read a 1,000-+-page legislative proposal or to natter on in this post if I didn’t believe that the future of our way of life is at stake. If you agree, please stand up and be counted by passing on this article to your friends. Here’s a live link: http://annmonteith.com/page32/files/category-0022polinomics0022.html

I should start by admitting I have a bias against BIG: I don’t much care for big cities, big schools, big bureaucratic corporations, big hospitals, and — most of all — big government. My life experience has taught me that big entities beget big problems, and the bigger the problems, the more resistant they are to solutions — especially common-sense solutions.

I like small towns because problems are easier to define, and common-sense solutions seem to be easier to come by because you know whom to call, and volunteers are easier to motivate.

As an Army brat, I attended 12 schools, including 4 high schools — one big one and three small ones. As both a student then and later as a teacher, I concluded that small schools are likely to serve students and parents better than their large, bureaucratic counterparts.

Large corporations become bureaucratic, almost by definition; and bureaucracy helps to obscure bad business practices. Just look at the recent history of financial institutions that did catastrophic damage, then were deemed by government as “too big to fail,” thus necessitating taxpayer bailouts and government takeovers.

When it comes to health care, I prefer to deal with routine issues at a small private practice in the tiny Maryland community where we have a lake house: The doc listens to you and the problem gets resolved. I even made the three-and-a-half-hour trip to that community to have an angry gall bladder removed because they could take me right away, rather than wait for at least two weeks to schedule the surgery at the huge Hershey Medical Center, which is only 7 miles from my Pennsylvania home. I’m glad the med center is there when big medical guns are needed; but it takes way too much energy to get a hangnail diagnosed there.

The remedy or the disease?

And now the Federal government, which has grown at a breathtaking pace since last fall, is poised to nationalize our health care system, according to a plan that, in effect, points to a leak in the national faucet and proposes to fix it by tearing up the entire American plumbing system. And just wait until you see the proposed bureaucratic solution. I’m certain that most Americans want health care reform that would address cost escalation, insurance for pre-existing conditions, portability, and catastrophic care. But this proposal redefines Byzantine complexity. The idea that healthcare, would become less complicated and more affordable by saddling it up this mind-numbing bureaucracy beggars belief. Take a look at how it is organized:

This diagram was created by Rep. Kevin Brady (R-Texas) and Republican staff of the Joint Economic Committee to illustrate the organization of the Democratic health care plan. It interested me because Republicans are being vilified for opposing the bill. I’m a registered Independent because neither party represents enough of my core views to strongly identify with, but on this one, I’m grateful to the Republicans for standing firm and to the Blue Dog Dems who are risking the ire of the White House in repudiating this nightmare.

Democrats have prevented Republican House Members from sending their constituents a mailing that includes this organization chart under House franking privileges, claiming that it is inaccurate. Well, I don’t think so because I’ve read the bill. In fact, I’m not sure it fully includes all of the plan’s complexity. Don’t take my word for it . . . you can read the thing yourself by clicking here.

Read the Bill!

Start by reading the Table of Contents; it is scary unto itself. Next: read pages 22-28, just to get a feel for the kinds of rules and regulations this monstrosity proposes. Lawyers will love it. Here are just a few page-by-page highlights to whet your appetite:

Page 27 covers “Health Insurance Exchanges,” which effectively brings private heath care under government control. See page 84, line 4 to see how sweeping this governmental mandate is and the potential it holds for rationing care.

Page 29, lines 4-16 establishes a cost-for-benefits ceiling (annual limitation) on “essential benefits” for what the government deems to be an acceptable plan.

Page 30, Section 123, line 11 mandates a private/public Health Benefits Advisory Committee government committee that decides what determines eligible treatments/benefits are provided by an acceptable plan.

Page 42 lays out the duties of the Health Choices Commissioner. He gets to choose your benefits, not you.

Page 50, Section 152: I’m pretty sure that the language of this section provides health care to non-US citizens, illegal or otherwise, even though another section of the bill says that it (not the section on page 50) doesn’t provide care to illegals. Consult your legal staff to find out for sure.

Page 65, Section 164 greatly expands subsidized care to retirees (55 years or older) and family members, even if they already have health plans. And wait until you read the red tape required to collect!

Page 143: Read Subtitle B of this section carefully, as it relates to “Employer Responsibility.” In it you will find that in order to “comply” employers must:

- Offer coverage to all employees and their families through the government option or a current employment-based health care plan.

- Be taxed at a rate of 8% of payroll if health care option is not offered to employees and dependents. Small businesses will pay less than 8%, but just imagine the increased costs involved for the private sector.

- Enrollment by employer of employee is automatic unless the employee opts out during a 30-day period. Unless the employee is covered by a family plan elsewhere, he or she will be subject to “Individual Responsibility” provisions, which the government dictates (see page 167, line 18 for “Tax on Individuals Without Acceptable Health Care Coverage.” Hint: They will be taxed at a rate of 2.5% of income.

- Pay special attention on page 150, line 8: “Special Rules for Small Employers, as this would pertain to most photographers (payroll under $400,000). If payroll is between $251,000 and $400,00 payroll tax will be 2-6%.

Page 57, Section 163 deals with Standardizing Electronic Administration Transactions. This looks scary to me because page 28, line 5 allows “real time determination of an individual’s financial responsibility at the point of service.” Sounds like governmentspeak for “we can get a look at your bank account.” I could be wrong. Hope so, especially since the it also enables electronic fund transfers to allow “automatic reconciliation,” which means the government now has direct access to your bank account. Imagine the outcry if George W. Bush had a bill on the Hill that would allow this level of government intrusion.

What about YOUR doctor?

Are you wondering how your doctor would be affected? Start on page 238, and I dare you to read through page 255. If you do, you’ll wonder why ANYONE would want to become a doctor (especially since the government decides on his or her level of reimbursement on page 127). My personal favorite of all the dictates is on page 253, line 10, under “Validating Relative Value Units” for doctors’ fee schedules: “Work elements to be validated include: time, mental effort and professional judgement, technical skill and physical effort, and stress due to risk.” OMG.

Page 265 covers government mandates on productivity for private health care; Page 489, Section 1308 allows the government to include Marriage and Family Therapy as a health care element; and on and on it goes. Believe me there are HUNDREDS of radical bureaucratic proposals in this bill, but I don’t have enough time to list all the catastrophes. Don’t take my word for it: Read it yourself, or to make it easier, divide it up among your friends and let them take notes, then exchange information.

Over recent months, I’ve watched as Congress and the Administration have severely limit the economic freedom of Americans by quadrupling the deficit, printing money to purchase our own debt, and delivering a pork-laden, non-stimulative “stimulus” bill, all of which are likely to prolong the recession. But in spite of this and a now-stalled cap-and-trade bill that is enough to scare the pajamas off of manufacturers from bread bakers to bomb makers, in the back of my mind I’ve believed there was still room for the private sector to restart the country’s economic engines, something that government cannot do.

An affordable bill? Not so much.

But this so-called health care “affordability” act, which will fundamentally alter one-sixth of our economy, could literally sink the ship of state. The administration says it will be revenue neutral; the Congressional Budget Office (which effectively works for the Democrats), says it will cost $1 trillion or more (think MORE) over 10 years. A growing number of Americans are seeing it for what it is: a naked government power grab based on the assumption that somehow government can do better in “caring for” people than they can do for themselves and through the private sector. This issue is far too serious to stay on the sidelines, so here are some things you can do to stop this national catastrophe:

- Call the local office of your U.S. Congressman and ask for an appointment over the August recess. DO IT NOW!!!

- Get your friends together and crowd into his or her local office. Politicians do pay attention when real live constituents speak to them politely and plainly.

- Bring signs and take pictures outside of his or her office, then send them to your local media, along with a few of your objections to the plan.

Common-sense reform

Yes, health care needs reform badly, but let’s start with a common-sense approach that tackles the issues that drive up costs:

- Separate routine care, catastrophic care, chronic care, and diagnostics to see what % of GDP they take up, and how much each is rising per annum. The costs of routine care are easier to reform; look for best-practice models for chronic care (including end-of-life care) and diagnostics; then let’s see where the cost differentials fall for catastrophic care, which might require a Federal option for uninsurable Americans, rather than unfunded mandates for the states.

- Give the responsibility for routine care (and perhaps diagnostics) back to individuals, allowing individuals to purchase routine health plans or tax-exempt savings plans that include diagnostics and catastrophic care as necessary elements unless and until we find a better way.

- Allow individuals to deduct health care plans to put them on the same par as businesses.

- Allow professional associations to form health care plans. Professional Photographers of America and other trade associations came very close to passing legislation in both houses of Congress several years ago. Estimates at the time were that this plan would cover 70% of uninsured Americans.

- Attack the physician-shortage issue. Does it make sense that there are more than half again as many lawyers in the U.S. than there are doctors? Only to lawyers who love to sue doctors, I suspect.

- President Obama has already said he will not support tort reform, but don’t give up on this.

Get these initiatives moving, then see what a government program for uninsured Americans would look like.

Please understand that I wouldn’t have taken the time to read a 1,000-+-page legislative proposal or to natter on in this post if I didn’t believe that the future of our way of life is at stake. If you agree, please stand up and be counted by passing on this article to your friends. Here’s a live link: http://annmonteith.com/page32/files/category-0022polinomics0022.html

Comments

Confessions of an Economic Conservative

20/09/15 19:29

Originally published on March 3, 2009

Since I was a child I’ve been bullish about small business: By age six I was hand crafting woven potholders and selling them from door to door. A born entrepreneur, I guess, I instinctively understood that if I wanted to achieve a higher standard of living than what was afforded to me by the meager $.50 a week allowance my parents provided, I would have to get off my butt and learn how to earn money by my wits. Some 500 pot holders later, I was committed to the romance of entrepreneurship. By high school I had a part-time job in a department store, so that I could start saving for a VW bug. During college I earned $.50 a page typing manuscripts and term papers for fellow English majors and worked summers as a typist for an Intelligence branch of the government. I thought the Signals Intelligence job would be exciting, but all I did was transcribe tapes forwarded to the Army by a chronically inebriated operative whose job it was to map all of the public phones in Jamaica. This was my first taste of government waste . . . one that required a Secret clearance no less!

By then a streak of 60’s idealism convinced me that I wanted to become a senior high school English teacher, and my work-study experience teaching 11th and 12th grade English exceeded my hopes that I could make a difference in the lives of kids by exposing them to the power of language. This sense of purpose didn’t last long, as I quickly ran afoul of the local branch of the Pennsylvania State Teacher’s Association. A representative informed me that the union did not look kindly on how many hours I was spending after school helping students and meeting with parents, as it put undue pressure on regular teachers to do the same. I also received information on the union’s political positions, which included opposing English as the official language of the U.S., a position that in good conscience I could never support because I believe so strongly in the need for a common language as vital cultural glue.

So much for idealism . . .

By the time Jim finished his MBA studies at Wharton and we got married and moved to Annville, it was obvious that if I didn’t agree to join the teacher’s union my life as a public school teacher would be made miserable, so I decided to apply for a position at a local college; I wasn’t looking for a fight in those days. Many years later I would run up against the union again—during a eight-year foray into education politics—during which the confrontation escalated from slashed tires to death threats and finally to a physical attack by a union rep, which led to his arrest. But that’s a story for another day.

The local college hired me as director of publications (I was grossly under qualified, so I had to learn while on the job), and later I was promoted to director of public relations. These jobs allowed me to finagle myself back into the classroom as a part-time journalism instructor, advisor to the school yearbook, and manager of several community internship projects involving English majors. All the while I also did part-time feature writing for the Harrisburg newspaper, which allowed me to illustrate my stories with my own photographs. I had begun learning photography from Jim, who had become a hobbyist in graduate school, as well as from a very talented student photographer with the yearbook. When I won a local newspaper’s Kodak snapshot contest, I was convinced I had what it takes to be a pro.

An original soccer mom?

By the mid-1970s I was one of the few moms who kept on working after having kids, and my after-hours writing and photography jobs allowed me to purchase more equipment. I looked forward to the day when I could quit my job at the college and build a small studio in a garage that sat on the farm property where we lived. I guess you could say that I was one of the very first “soccer moms.” Those plans changed dramatically when Jim came home one fine fall day several years later and announced that he had decided to quit his well-paying job as general manager of a plastics company to help me start up my photography business that he now intended to join. That decision, which I fully supported, set into motion a series of events that severely jeopardized our then pleasant way of life and hopes for the future. In the process, I learned a lot about the banking industry.

Most of my business students know the story of how I came to owe $187,000 at 23% interest because of the bad decisions we made investing borrowed money at a time when America’s banking system was out of control and inflation threatened every family’s way of life. During this period, many hard-working farmers lost land that had been in their families for generations. Fund-raisers were held around the world for these American farmers, who, like anyone who borrowed money during this period, had been victimized by banks and savings-and-loan institutions that racked up commissions by convincing farmers and others like Jim and me to keep on borrowing because the value of our land was escalating, and it represented the vehicle by which we should fulfill our dreams. When regulators got nervous about this frenzy, lending institutions began calling in loans, and the house of cards began to collapse, precipitating what became known as the Savings and Loan Crisis. If you want to read some history about the origin and effects of this debacle, click here. It illustrates that we’ve been down this path before, and it begs the question: Why are we repeating it again?

Surviving economic disaster

Jim and I were among the fortunate few who survived this bleak period by liquidating personal assets and working double shifts in the studio so that we could pay down debt. Early on I was fortunate enough to meet the late Bud Haynes, who became my business mentor; he made me understand that creating a business could be every bit as creative and rewarding as making photographs. Eventually, Bud recruited me to teach with him, which developed in me a sense of calling because of my gratitude to him and other PPA instructors who helped our business to succeed. Furthermore, I had learned so much from the School of Hard Knocks that I wanted to do what I could to help others from making bad business decisions. The experience also strengthened my awareness of the importance of sticking to fundamental business principles such as the importance of staying out of debt, creating a plan for every aspect of your business, and practicing fiscally conservative oversight in all affairs of business and personal finance. Having watched so much harm come from government manipulation of markets also hardened my belief in the wisdom of allowing free markets to function, even if it creates financial pain and hardship. Unfortunately pain sometimes is the ONLY path to wisdom and progress.

If you’re still reading, I want you to know that I’ve recounted this personal history as an explanation as to why I have more than a passing interest in the state of our economy. When the banking system began to implode last fall, I began using what little spare time I had to learn more about the worldwide banking system. The more I studied, the more convoluted the subject became, and I began to understand how a nerdy guy like Bernie Madoff (whom the media inexplicably calls “charming”) could cheat his clients out of so many zillions of dollars: When so few people understand the complexities of international banking, you can get away with almost anything . . . until the Ponzi scheme finally plays out.

One thing has become abundantly clear to me: The same kinds of greedy manipulators who orchestrated the Savings and Loan debacle were alive and well and flourishing in the 21st century, and if you peeked into their business plans, you could find government lending a helping hand. I have no doubt that government bureaucrats (under both Clinton and Bush by the way) had very good intentions in promoting and tolerating sub-prime loans: They wanted to increase home ownership, a noble ideal to be sure. I doubt if they envisioned the spectacle of houses replacing land as the new free ride to the top. I’m sure they regret cracking open the door for lenders with visions of non-stop commission checks to break it down.

Bad behavior with the color of money

As an unabashed advocate of free enterprise, it has been discomforting to witness the parade of capitalists — especially those in the financial sector — behaving so badly; but I am mindful that layers upon layers of government bureaucracy make it so much easier for bad financial behavior to go unnoticed. It is instructive to note that it wasn’t the FBI that “got their man” with Bernie Madoff; his sons turned him in when his evil house of cards began to flutter. With a few more layers of bureaucracy, perhaps old Bernie would still be in business “spreading the wealth.”

So for the last four months I’ve been looking to see which way government would go in addressing our financial crisis. The years I spent in education politics made me fairly cynical about politicians on both sides of the aisle. It’s sometimes hard to tell a Republican from a Democrat these days or even to determine if there is a “center” operating anywhere in the political spectrum. I’ve been watching closely and hopefully, but the recent unveiling of a so-called stimulus package, followed up by the pork-laden omnibus spending bill that represents an all-out assault on the business sector, which has set me to emailing and calling my elected representatives. Their mindless responses have not lifted my spirits.

So what’s next?

At this writing our government seems hell-bent on repeating the mistakes of the past: thinking the government can supplant the private sector, and by sheer force of will and taxation to reverse what it helped to cause, using the same tactics that precipitated the problem in the first place: spending money we don’t have to subsidize failing institutions; borrowing from nations who may not have our best interest at heart; and targeting the “rich,” so that government can orchestrate the next rocketing bubble that will do what all bubbles eventually do: burst when they have wreaked maximum havoc.

So Attention My Government: Please recognize that it is not government — rather it is the private sector —that powers economic progress in America: Encourage us, then get out of our way! Don’t tell us you will punish us if we get rich. Most small business owners, such as photographers, will never hit that magic $200,000 + income level in the proposed Tax Code revisions where the government will start lowering deductions for state and local taxes, mortgages, and most cynical of all . . . charitable contributions. Just the specter of economic punishment will rob small business people of the desire to take risks. As an economic growth strategy, these current government proposals are about as foolish as trying to strangle a hen in order to make her lay more eggs.

Reading about the budget’s provisions has made me wonder what I would be doing today if my parents had not encouraged me to sell potholders door to door when I was six years old. What if they had told me that I could do it, but I had to give them more than half of what I earned? I suspect that single act would have robbed me of the great gift of Hope.

When the history is written . . .

I don’t much like labels, but I am just fine with being called an economic conservative, because most of us who identify with this mindset believe that if it looks too good to be true . . . it simply IS too good to be true. We tend to trust what we know to be true from personal experience and what we can learn from history. When Enron collapsed, I studied the reasons why. The reasons no longer matter: What I learned is that if a company cannot explain to you what it does to earn money in less than three sentences, then you should not go to work for it or invest in it. What I’ve learned so far about accumulating wealth is that is fine to want to get rich, but the best strategy is to get rich SLOWLY! And you’d better have a plan to do so. What I’m afraid I will be studying in the years to come is what happened when the government couldn’t explain its economic recovery plan in less than 1,000 pages and the Congress voted it through the day they received it without reading it.

I feel better now that I have gotten all this off my chest. I’m finding that writing about my concerns is cathartic. I don’t know whether I’ll write about this subject again, but if I do, I promise to keep it shorter (well maybe a little shorter). I’m learning every day, and perhaps I’ll pass on some of the resources I’m looking at in case anyone out there is interested.

Since I was a child I’ve been bullish about small business: By age six I was hand crafting woven potholders and selling them from door to door. A born entrepreneur, I guess, I instinctively understood that if I wanted to achieve a higher standard of living than what was afforded to me by the meager $.50 a week allowance my parents provided, I would have to get off my butt and learn how to earn money by my wits. Some 500 pot holders later, I was committed to the romance of entrepreneurship. By high school I had a part-time job in a department store, so that I could start saving for a VW bug. During college I earned $.50 a page typing manuscripts and term papers for fellow English majors and worked summers as a typist for an Intelligence branch of the government. I thought the Signals Intelligence job would be exciting, but all I did was transcribe tapes forwarded to the Army by a chronically inebriated operative whose job it was to map all of the public phones in Jamaica. This was my first taste of government waste . . . one that required a Secret clearance no less!

By then a streak of 60’s idealism convinced me that I wanted to become a senior high school English teacher, and my work-study experience teaching 11th and 12th grade English exceeded my hopes that I could make a difference in the lives of kids by exposing them to the power of language. This sense of purpose didn’t last long, as I quickly ran afoul of the local branch of the Pennsylvania State Teacher’s Association. A representative informed me that the union did not look kindly on how many hours I was spending after school helping students and meeting with parents, as it put undue pressure on regular teachers to do the same. I also received information on the union’s political positions, which included opposing English as the official language of the U.S., a position that in good conscience I could never support because I believe so strongly in the need for a common language as vital cultural glue.

So much for idealism . . .

By the time Jim finished his MBA studies at Wharton and we got married and moved to Annville, it was obvious that if I didn’t agree to join the teacher’s union my life as a public school teacher would be made miserable, so I decided to apply for a position at a local college; I wasn’t looking for a fight in those days. Many years later I would run up against the union again—during a eight-year foray into education politics—during which the confrontation escalated from slashed tires to death threats and finally to a physical attack by a union rep, which led to his arrest. But that’s a story for another day.

The local college hired me as director of publications (I was grossly under qualified, so I had to learn while on the job), and later I was promoted to director of public relations. These jobs allowed me to finagle myself back into the classroom as a part-time journalism instructor, advisor to the school yearbook, and manager of several community internship projects involving English majors. All the while I also did part-time feature writing for the Harrisburg newspaper, which allowed me to illustrate my stories with my own photographs. I had begun learning photography from Jim, who had become a hobbyist in graduate school, as well as from a very talented student photographer with the yearbook. When I won a local newspaper’s Kodak snapshot contest, I was convinced I had what it takes to be a pro.

An original soccer mom?

By the mid-1970s I was one of the few moms who kept on working after having kids, and my after-hours writing and photography jobs allowed me to purchase more equipment. I looked forward to the day when I could quit my job at the college and build a small studio in a garage that sat on the farm property where we lived. I guess you could say that I was one of the very first “soccer moms.” Those plans changed dramatically when Jim came home one fine fall day several years later and announced that he had decided to quit his well-paying job as general manager of a plastics company to help me start up my photography business that he now intended to join. That decision, which I fully supported, set into motion a series of events that severely jeopardized our then pleasant way of life and hopes for the future. In the process, I learned a lot about the banking industry.

Most of my business students know the story of how I came to owe $187,000 at 23% interest because of the bad decisions we made investing borrowed money at a time when America’s banking system was out of control and inflation threatened every family’s way of life. During this period, many hard-working farmers lost land that had been in their families for generations. Fund-raisers were held around the world for these American farmers, who, like anyone who borrowed money during this period, had been victimized by banks and savings-and-loan institutions that racked up commissions by convincing farmers and others like Jim and me to keep on borrowing because the value of our land was escalating, and it represented the vehicle by which we should fulfill our dreams. When regulators got nervous about this frenzy, lending institutions began calling in loans, and the house of cards began to collapse, precipitating what became known as the Savings and Loan Crisis. If you want to read some history about the origin and effects of this debacle, click here. It illustrates that we’ve been down this path before, and it begs the question: Why are we repeating it again?

Surviving economic disaster

Jim and I were among the fortunate few who survived this bleak period by liquidating personal assets and working double shifts in the studio so that we could pay down debt. Early on I was fortunate enough to meet the late Bud Haynes, who became my business mentor; he made me understand that creating a business could be every bit as creative and rewarding as making photographs. Eventually, Bud recruited me to teach with him, which developed in me a sense of calling because of my gratitude to him and other PPA instructors who helped our business to succeed. Furthermore, I had learned so much from the School of Hard Knocks that I wanted to do what I could to help others from making bad business decisions. The experience also strengthened my awareness of the importance of sticking to fundamental business principles such as the importance of staying out of debt, creating a plan for every aspect of your business, and practicing fiscally conservative oversight in all affairs of business and personal finance. Having watched so much harm come from government manipulation of markets also hardened my belief in the wisdom of allowing free markets to function, even if it creates financial pain and hardship. Unfortunately pain sometimes is the ONLY path to wisdom and progress.

If you’re still reading, I want you to know that I’ve recounted this personal history as an explanation as to why I have more than a passing interest in the state of our economy. When the banking system began to implode last fall, I began using what little spare time I had to learn more about the worldwide banking system. The more I studied, the more convoluted the subject became, and I began to understand how a nerdy guy like Bernie Madoff (whom the media inexplicably calls “charming”) could cheat his clients out of so many zillions of dollars: When so few people understand the complexities of international banking, you can get away with almost anything . . . until the Ponzi scheme finally plays out.

One thing has become abundantly clear to me: The same kinds of greedy manipulators who orchestrated the Savings and Loan debacle were alive and well and flourishing in the 21st century, and if you peeked into their business plans, you could find government lending a helping hand. I have no doubt that government bureaucrats (under both Clinton and Bush by the way) had very good intentions in promoting and tolerating sub-prime loans: They wanted to increase home ownership, a noble ideal to be sure. I doubt if they envisioned the spectacle of houses replacing land as the new free ride to the top. I’m sure they regret cracking open the door for lenders with visions of non-stop commission checks to break it down.

Bad behavior with the color of money

As an unabashed advocate of free enterprise, it has been discomforting to witness the parade of capitalists — especially those in the financial sector — behaving so badly; but I am mindful that layers upon layers of government bureaucracy make it so much easier for bad financial behavior to go unnoticed. It is instructive to note that it wasn’t the FBI that “got their man” with Bernie Madoff; his sons turned him in when his evil house of cards began to flutter. With a few more layers of bureaucracy, perhaps old Bernie would still be in business “spreading the wealth.”

So for the last four months I’ve been looking to see which way government would go in addressing our financial crisis. The years I spent in education politics made me fairly cynical about politicians on both sides of the aisle. It’s sometimes hard to tell a Republican from a Democrat these days or even to determine if there is a “center” operating anywhere in the political spectrum. I’ve been watching closely and hopefully, but the recent unveiling of a so-called stimulus package, followed up by the pork-laden omnibus spending bill that represents an all-out assault on the business sector, which has set me to emailing and calling my elected representatives. Their mindless responses have not lifted my spirits.

So what’s next?

At this writing our government seems hell-bent on repeating the mistakes of the past: thinking the government can supplant the private sector, and by sheer force of will and taxation to reverse what it helped to cause, using the same tactics that precipitated the problem in the first place: spending money we don’t have to subsidize failing institutions; borrowing from nations who may not have our best interest at heart; and targeting the “rich,” so that government can orchestrate the next rocketing bubble that will do what all bubbles eventually do: burst when they have wreaked maximum havoc.

So Attention My Government: Please recognize that it is not government — rather it is the private sector —that powers economic progress in America: Encourage us, then get out of our way! Don’t tell us you will punish us if we get rich. Most small business owners, such as photographers, will never hit that magic $200,000 + income level in the proposed Tax Code revisions where the government will start lowering deductions for state and local taxes, mortgages, and most cynical of all . . . charitable contributions. Just the specter of economic punishment will rob small business people of the desire to take risks. As an economic growth strategy, these current government proposals are about as foolish as trying to strangle a hen in order to make her lay more eggs.

Reading about the budget’s provisions has made me wonder what I would be doing today if my parents had not encouraged me to sell potholders door to door when I was six years old. What if they had told me that I could do it, but I had to give them more than half of what I earned? I suspect that single act would have robbed me of the great gift of Hope.

When the history is written . . .

I don’t much like labels, but I am just fine with being called an economic conservative, because most of us who identify with this mindset believe that if it looks too good to be true . . . it simply IS too good to be true. We tend to trust what we know to be true from personal experience and what we can learn from history. When Enron collapsed, I studied the reasons why. The reasons no longer matter: What I learned is that if a company cannot explain to you what it does to earn money in less than three sentences, then you should not go to work for it or invest in it. What I’ve learned so far about accumulating wealth is that is fine to want to get rich, but the best strategy is to get rich SLOWLY! And you’d better have a plan to do so. What I’m afraid I will be studying in the years to come is what happened when the government couldn’t explain its economic recovery plan in less than 1,000 pages and the Congress voted it through the day they received it without reading it.

I feel better now that I have gotten all this off my chest. I’m finding that writing about my concerns is cathartic. I don’t know whether I’ll write about this subject again, but if I do, I promise to keep it shorter (well maybe a little shorter). I’m learning every day, and perhaps I’ll pass on some of the resources I’m looking at in case anyone out there is interested.